Oregon has a sophisticated trust code and a strong legal framework for fiduciary administration.

While for most clients, an Oregon-situs trust remains the right solution, clients with certain planning objectives— particularly around taxation, dynasty planning, directed trusts, and asset protection—may wish to consider a Nevada trust administered by a professional, independent trustee.

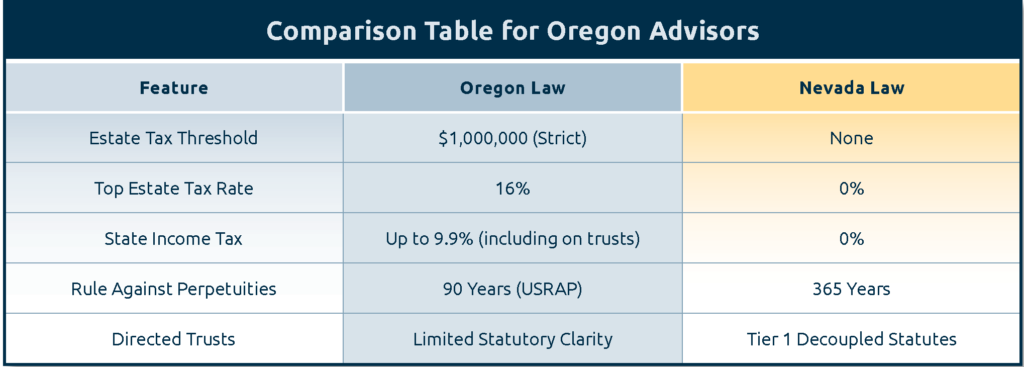

Why Nevada? Oregon’s Uniform Trust Code is robust. What’s the real delta?

While Oregon offers a stable legal framework, Nevada provides Tier 1 statutory advantages that Oregon’s UTC does not address—specifically regarding taxation and perpetuities. Most notably, Oregon imposes a high state income tax (up to 9.9%) on non-grantor trusts. Nevada imposes no state income tax, providing a significant “tax alpha” for trusts accumulating income or rebalancing portfolios. Furthermore, while Oregon’s Rule Against Perpetuities is generally limited to 90 years (USRAP), Nevada permits 365-year dynasty trusts, allowing Oregon families to avoid the 10%–16% Oregon Estate Tax across multiple generations.

Can an existing Oregon trust be decanted into a Nevada trust without court involvement?

In many cases, yes. While Oregon’s decanting statutes (ORS 130.540) are functional, Nevada’s decanting laws are among the most flexible in the nation. If a trustee has discretionary distribution authority, our Nevada charter can often decant assets into a new Nevada trust to modernize administrative provisions and enhance asset protection—frequently without judicial approval or the “notice to the Attorney General” hurdle required by Oregon law.

What’s your view on Nevada Incomplete Gift Non-Grantor (NING) trusts for Oregon residents?

NINGs are a primary driver for Oregon practitioners seeking a Nevada charter. For Oregon residents facing a significant liquidity event—such as the sale of a business or a concentrated stock position—a NING may mitigate Oregon’s 9.9% top-tier income tax. We provide the Nevada situs, independent trustee, and administrative substance required to support non-grantor status. Given Oregon’s aggressive tax stance, we coordinate closely with tax counsel to ensure these structures meet the “substantial personal presence” and “substance” requirements.

How does Nevada’s Domestic Asset Protection Trust (DAPT) compare to Oregon law?

Oregon does not have a robust self-settled spendthrift (DAPT) statute. Nevada, however, is consistently ranked as the #1 DAPT jurisdiction in the U.S. Key advantages include a short two-year statute of limitations on fraudulent transfer claims and the absence of “exception creditors” (like alimony or child support) that exist in other states. For Oregon clients in high-risk professions, moving the “situs of protection” to Nevada is a significant upgrade.

Oregon’s estate tax threshold is only $1 million. How does a Nevada Dynasty Trust help ‘freeze’ that exposure?

Oregon has the lowest estate tax threshold in the country, and unlike the federal system, it is not indexed for inflation. This creates an “inflation tax” on Oregon families.

By transferring assets into a Nevada Dynasty Trust, an Oregon resident can “freeze” the taxable value of those assets at the time of the gift.

Avoid Successive Taxation: In Oregon, assets are typically taxed at each generational death. A Nevada Dynasty Trust can last up to 365 years. Once assets are in the trust, they are never subject to Oregon estate tax again as they pass from children to grandchildren and beyond.

Capturing Growth: All future appreciation on those assets occurs outside of the grantor’s and the beneficiaries’ Oregon taxable estates. For a client with a high-growth business or real estate portfolio, this “freeze” can save millions in state taxes over several decades.

Can you accommodate Directed Trusts? Can my client keep their existing RIA?

Yes—this is a core strength of Nevada trust law. Nevada’s Directed Trust statutes explicitly allow for the bifurcation of fiduciary duties. As Administrative Trustee, we handle trust administration, reporting, distributions, and compliance, while the client’s chosen RIA or Investment Committee retains full investment authority. This structure preserves advisor relationships, limits fiduciary liability creep, and keeps each party operating squarely within their expertise.